Completing a bottom up approach (looking at past receipts, bank statements, etc) to figuring out your expenses and spending is a key part about this next step--taking a top down approach of to building a spending model to control what your spending should be. They should really meet in the middle. Any model will have certain assumptions, but they need to be realistic for the model to be useful. A top-down budget model that isn't achievable or aligned to your lifestyle and goals is just an exercise in frustration.

This spending model should not only accurately depict non-discretionary and fixed expenses, debt payments, and savings, but also capture things like eating out, entertainment, shopping, and similar discretionary categories. I'd also recommend a reserve budget line (say 2-5%) for unknowns. The goal at this point is to arrive at a spending model (a budget, if you like) where your expenses are less than your income. Even if you can't get to that point, you'll now have a model for where your money is going so you can make informed decisions on where it should go.

The next step is for you to examine what you are spending and decide if it's in line with what you want to be spending. This is where you will begin to shape your spending model so that it captures the things/services/savings/investing that are necessary, meaningful and important to you and your goals. I can't know what's important to you, and we don't yet know what the savings amount should be (though hopefully it's > 0, but we'll get to that, and it depends on any debt you have), but what's important at this point is to know where your money is going, have a basic top-down spending model that you can use to make conscious and informed decision about what you want your money doing for you. Remember, that money was hard-earned--you exchanged a portion of the time you have left on this earth for it. Make the most of that exchange.

Next, we'll look in more detail at optimizing that spending model.

Sunday, December 7, 2014

Saturday, December 6, 2014

Checkout the charities you donate to--some questions about Red Cross accounting

A reminder to checkout the charities you might donate to this year. There are some questions about how the Red Cross is accounting for its contributions and expenses:

Here's the Red Cross Response:

I don't have enough information to know who is exactly right, but either way, I encourage you to examine the charities you might donate to. Charity Navigator is a good source (they pretty much agree with the Red Cross accounting of expenses, by the way)

Via propublica.org"The American Red Cross regularly touts how responsible it is with donors' money. "We're very proud of the fact that 91 cents of every dollar that's donated goes to our services," Red Cross CEO Gail McGovern said in a speech in Baltimore last year. "That's world class, obviously."McGovern has often repeated that figure, which has also appeared on the charity's website. "I'm really proud" that overhead expenses are so low, she told a Cleveland audience in June.

The problem with that number: It isn't true."

Here's the Red Cross Response:

"We firmly stand by the fact that an average of 91 cents of every dollar the American Red Cross spends is invested in humanitarian services and programs. In a wide range of our materials- including donor stewardship reports and publicly available financial statements, the Red Cross has used the wording that an average of 91 cents of every dollar the Red Cross spends is invested in humanitarian services and programs. This has been a long term practice for the Red Cross.

There are some instances where the language used has not been as clear as it could have been, and we are clarifying that language. Asserting that this is an attempt to mislead the public is absolutely and unequivocally untrue."

I don't have enough information to know who is exactly right, but either way, I encourage you to examine the charities you might donate to. Charity Navigator is a good source (they pretty much agree with the Red Cross accounting of expenses, by the way)

Really interesting US Currency Design Idea--If not for this, how about for Savings Bonds or Passports?

Pretty amazing design idea for U.S. Currency by Travis Purrington. I like paper cash for routine transactions--it's fast and gives you a better sense of how much you are spending and how much you have to left to spend (it's whatever's left in your wallet).

While I think it's a long-shot to see this on actual U.S. Currency, how about on a U.S. Savings Bond--though paper bonds are being phased out and currently only available for tax refunds. Ok, then, how about U.S. Passports?

Article here, via foreignpolicy.com

Current U.S. Passports:

While I think it's a long-shot to see this on actual U.S. Currency, how about on a U.S. Savings Bond--though paper bonds are being phased out and currently only available for tax refunds. Ok, then, how about U.S. Passports?

Article here, via foreignpolicy.com

Photobook deal surprise--from Apple, who'd have guessed!

For the past several years we've purchased small Christmas photo books for family members. We have been satisfied with Mypublisher and Shutterfly over the years, and just made this year's order through Apple's iphoto.

We chose the 8 x 6 album totaling 10.61 (included free shipping through 12/12/14).

We chose the 8 x 6 album totaling 10.61 (included free shipping through 12/12/14).

$9.99

MEDIUM8×6 inches

20 pages

49¢/additional page

HP Stream--Possibly a Great Family Computer (and check out the deflation of computer prices!)

Here's an interesting idea if you or your family (especially the kids) are in need of a computer:

HP Stream 11 or HP Stream 13.  Check out what Paul Thurrott has to say. If my computers wear out or break to the point I can't fix them, I'd definitely by looking at something like this.

Check out what Paul Thurrott has to say. If my computers wear out or break to the point I can't fix them, I'd definitely by looking at something like this.

P.S., I recommend the Microsoft Store's Signature Edition of this. It doesn't have the extra trial software loaded on the other versions so it will run smoother.

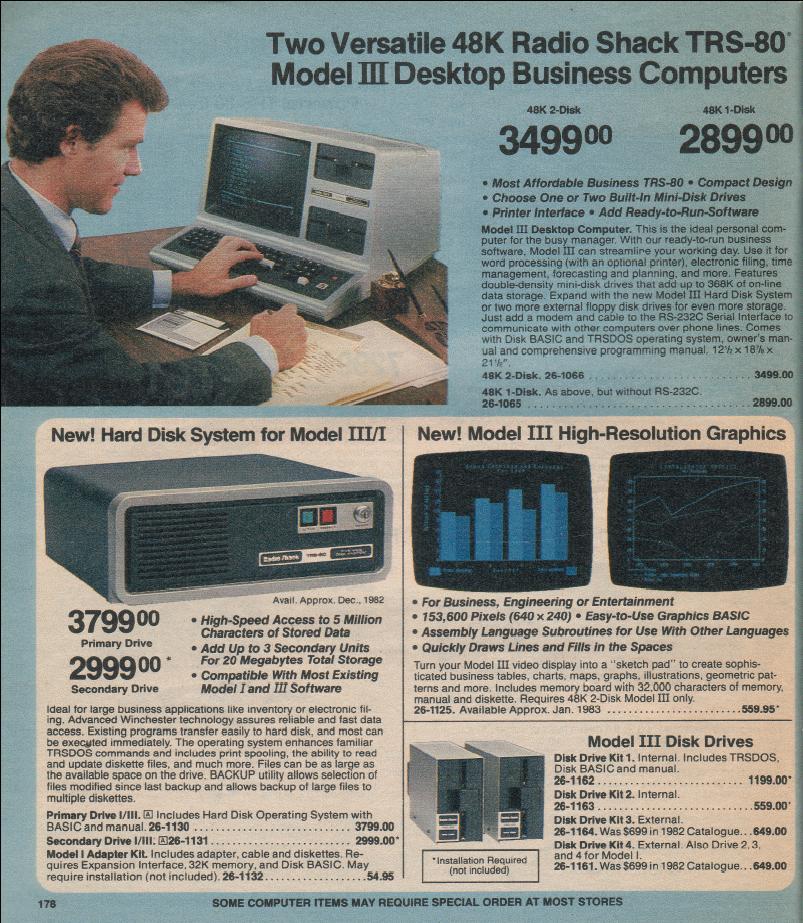

I'm amazed at the deflation in price and increase in performance I've seen in computers. Check out this 1983 ad for an old TRS-80:

Going, back further, take a look at IBM's typewriter prices. The Model B, below, went for $575 when first sold in 1954 (that's $5,075.24 in 2014 dollars!):

P.S., I recommend the Microsoft Store's Signature Edition of this. It doesn't have the extra trial software loaded on the other versions so it will run smoother.

I'm amazed at the deflation in price and increase in performance I've seen in computers. Check out this 1983 ad for an old TRS-80:

Going, back further, take a look at IBM's typewriter prices. The Model B, below, went for $575 when first sold in 1954 (that's $5,075.24 in 2014 dollars!):

Amazon's New Warehouse Robots

Warehouse robots=cool: Gurufocus.com, Amazon Robots To Make Your Christmas Happier

"Amazon.com has installed more than 15,000 robots across 10 U.S. warehouses; a move that promises to cut operating costs by one-fifth and move packages out of the door more quickly in the run-up to meet the Christmas shipment rush."

Another example of how Amazon is working to

reduce operating costs on the road to profitability. My view of Amazon is that they are trying to

grow sales while increasing efficiency of delivery system and gaining leverage

over suppliers in order to drive competitors out of business and eventually be profitable.

- Amazon may be willing to take losses for a very long time to gain market share and customers—this puts enormous pressure on their competitors.

- Amazon Prime is another very interesting and useful (from a consumer perspective) loss leader.

- How long can Walmart match Amazon’s prices while paying overhead and employee costs?

- On the other hand, how long can Amazon wait to be profitable? It’s been 20 years so far, so perhaps a while longer.

Walmart—probably has the best chance of competing with

Amazon online.

- Their store experience is very poor--crowded, dirty, not enough customer service or sales people--those there don't seem to be very motivated. Our family avoids Walmart stores at nearly all costs--we might go early in the morning, but never during prime shopping hours.

- Their online store is decent, prices are good, and ship to store could be useful, but there is still work to be done there. Did I mention I really don’t like walking into Walmart—it feels like I'm losing a small piece of my soul each time. What if they set up a drive through pickup? You’d order online, then drive to an area where someone would bring you what you ordered (like several grocery stores are doing). I’d much prefer to order from them online if I could avoid the experience of parking, walking into the store waiting in line at customer service to find someone to give me my order.

- I once ordered something, put down the wrong store for pickup, then found that the store my wife went to to pick it up for me couldn't fill the order (even though the item was on their shelves). She had to go across town to the other Walmart to pick it up. You could probably guess the feedback she had for me on that one. Walmart’s inventory/sales management tools should have been able to handle that easily--needless to say we haven't tried that again.

Target—store experience is much better than Walmart (less crowded, more and better help), can’t necessarily compete on price.

Leveraging online sales with positive store experience could be the

way. Still, they are struggling in the

revenue and are having a tough time with new stores in Canada. While their stock dividend is holding, their payout ratio is now way too high.

Barnes & Noble—similar to Target, they present a very good store experience,

but how many people browse Barnes & Noble, and then order a book from Amazon

either for delivery or for their Kindles? I can’t imagine their supply chain is anywhere

close to Amazon’s in terms of efficiency. Nor do I think they can handle extended unprofitably the way Amazon can.

- It’s tough to imaging Barnes and Noble being around another 10 years, but perhaps they’ll find a way.

- Tying the Nook to the Android/Google platform might be that way.

- Highlight that store experience--find people who will pay to sip coffee while browsing for books.

Begin by finding the starting conditions--Income and Expenses

Like any experiment or design study, you need to know the starting conditions. Looking at the expenses vs. income equation, you need to know where you are to make a model to help you plan for where you want to be.

Step 1: What's my income. I create a spreadsheet with all my income sources at the top. I split it out by paycheck, and then sum it up to see what it is each month. I don't include any investment income (dividends, interest, etc) because at this point I reinvest that. If your income varies by month, estimate at whatever time period you're most confident in--I'd look back at my last 2 years of paychecks and take the average. You could also take the standard deviation, to get a sense of how much income may vary.

Step 3: Track your spending over the last year if you have records that let you do so. If not, start tracking it over the next 1-3 months.

Step 1: What's my income. I create a spreadsheet with all my income sources at the top. I split it out by paycheck, and then sum it up to see what it is each month. I don't include any investment income (dividends, interest, etc) because at this point I reinvest that. If your income varies by month, estimate at whatever time period you're most confident in--I'd look back at my last 2 years of paychecks and take the average. You could also take the standard deviation, to get a sense of how much income may vary.

- Income before or after taxes? I use after tax income and deal with taxes separately. I find it gives me a better sense of what I have to work with. If you prefer, or if you have a more complicated tax situation (paying estimated taxes for instance), you might want to handle this differently.

- P.S., If you checked out that IRS link on estimated taxes, did you notice the language options: Chinese, Korean, Vietnamese, and Russian?--interesting what that might say about the demographics of small business owners or independent contractors

Step 3: Track your spending over the last year if you have records that let you do so. If not, start tracking it over the next 1-3 months.

- Don't be surprised if simply by tracking what you spend, you spend less in certain categories (i.e. did we really spend that much on going out to eat!). Knowing what you're spending and really feeling your money is a key part of this.

- You've traded your finite time for this money--you should feel something when you spend it; mindless spending likely means overspending on things that aren't meaningful to you.

- Feel free to adjust your categories as you go. The level of detail depends on how closely you want to track/model/control spending in a particular category.

- I like Quicken, but don't love it. It's gotten slower over the years, but it automates a substantial portion of my financial tracking and I have a lot of data captured with it, so I stick with the software.

- There are other options out there than many people recommend--I haven't tried them myself, but they might be useful. Your bank's website might also have useful tracking tools. Here are some ideas in no particular order:

Friday, December 5, 2014

A Great Day in Space

A great day for an engineer. Woke up and watched NASA launch the Orion Spacecraft on it's maiden flight. After the Space Shuttle's retirement, glad we're getting back on track to a manned space capability.

http://www.nasa.gov/press/2014/december/nasa-s-new-orion-spacecraft-completes-first-spaceflight-test/#.VIJXrzHF9q1

http://boingboing.net/2014/12/05/nasas-orion-launch-a-success.html

Also, lot's of exciting things going on in the private space sector:

NASA Commercial Crew Program

Virgin Galactic

http://www.nasa.gov/press/2014/december/nasa-s-new-orion-spacecraft-completes-first-spaceflight-test/#.VIJXrzHF9q1

http://boingboing.net/2014/12/05/nasas-orion-launch-a-success.html

Also, lot's of exciting things going on in the private space sector:

NASA Commercial Crew Program

Virgin Galactic

Translate Savings Into Income

I'm probably rediscovering what many have already, but as I think about financial independence, I'm thinking about my method for taking net worth and translating it into income. That's one half of the financial independence equation; the other is expenses).

There's many ways to have passive income do this:

- Withdraw savings

- Sell assets

- Bonds

- Dividend paying stocks

- Some type of passive business

Then I start thinking about, interest rates, safe withdrawal rate, dividend yields and what does this all mean. Here are a few things that are helping me figure this out. More to follow.

Your Money or Your Life

A Random Walk Down Wall Street

The Single Best Investment: Creating Wealth With Dividend Growth

Physics of Wall Street

Chowder on Seeking Alpha

Project 3 Million

Mr. Money Mustache

Treasury Direct: I-Bonds

There's many ways to have passive income do this:

- Withdraw savings

- Sell assets

- Bonds

- Dividend paying stocks

- Some type of passive business

Then I start thinking about, interest rates, safe withdrawal rate, dividend yields and what does this all mean. Here are a few things that are helping me figure this out. More to follow.

Your Money or Your Life

A Random Walk Down Wall Street

The Single Best Investment: Creating Wealth With Dividend Growth

Physics of Wall Street

Chowder on Seeking Alpha

Project 3 Million

Mr. Money Mustache

Treasury Direct: I-Bonds

Welcome to Engineer Net Worth

Welcome to Engineer Net Worth--a place where I'll collect my ideas, interests, and links to information related to engineering your own net worth. I'm an engineer by inclination and training, and so I approach my finances in a similar way. I'm model and data driven and think methodically. I want to collect a lot of ideas and information, then form my own views in a way that makes sense to me.

My goal is financial independence as early as possible with a high quality and best value way of life. As I work toward that goal, I'll share ideas and links to information that I think is helpful, interesting, or thought provoking.

My goal is financial independence as early as possible with a high quality and best value way of life. As I work toward that goal, I'll share ideas and links to information that I think is helpful, interesting, or thought provoking.

Subscribe to:

Comments (Atom)